The Bear Case against Philip Falcone, Harbinger Group Inc, and Spectrum Brands

Three Parts:

Three Parts:

1.

Philip

Falcone

2. Harbinger Group Inc (NYSE:HRG)

Last 9.71

Mkt cap 1.36B

P/E -

52 week 2.75 - 10.85

3. Spectrum Brands Holdings, Inc.(NYSE:SPB)

Last 47.50

Mkt cap 2.44B

P/E 275.99

52 week 23.04 - 48.22

Part

1: Philip Falcone

When it comes to stock manipulation Philip Falcone has the

magic. It was only back in June that we

saw the headline “Philip A. Falcone and Harbinger Charged with Securities

Fraud.” Shortly before that he made news

for losing billions of his investor’s money in LightSquared, a trade so rouge

it reeks of foul play. (Read Pages 170-175 and let me know if this sounds familiar The Book of Daniel Drew)

I found the SEC report against Falcone to be a real delight

and suggest if you’re interested in gaining insight into the ethics of Mr

Falcone, you click the links found here.

Otherwise

here are a couple highlights:

- Falcone fraudulently obtained $113.2 million from a hedge fund that he advised and misappropriated the proceeds to pay his personal taxes;

- Falcone and Harbinger secretly offered and granted favorable redemption and liquidity rights to certain strategically-important investors in exchange for those investors’ consent to restrict redemption rights of other fund investors, and concealed the arrangement from the fund’s directors and investors;

- Harbinger engaged in illegal trades in connection with the purchase of common stock in three public offerings after having sold the same securities short during a restricted period.

On the matter of the alleged 113.2 million

loan for Falcone's “personal taxes”, I found this quote from the SEC report

rather odd.

"The Defendants also never contacted any

state or federal tax authorities, such as the Internal Revenue Service". sec.gov/litigation/

Huh? Wouldn't it seem logical that a person would do this first? Which is why I'm especially curious if the SEC confirmed

with the IRS that Philip Falcone did in fact have a 113.2M tax liability due in

October 2009.

Falcone refused to accept

a bank loan to cover his liability because it required him to pledge personal

assets (House, Art, estate on St. Barts Residence etc), which I found strange too...as long as you didn't have ill-intentions, what would be the problem?

Instead Falcone tried using fund interests as

collateral but,

"Jenson had been unable to find any bank

that was willing to lend at any price against Falcones SSF interests." sec.gov/litigation/

Boy, it really speaks volumes about the

quality of the underlying assets when the Banks who underwrote many of the

deals and whom Falcone has done billions in transactions with refuse to lend

against Falcones stake in the fund.

Rather than pledge personal assets for the “IRS tax liability”, Falcone arranged a personal loan from one of his funds. This did not go over well for several reasons, 1) The fund had halted redemptions, 2) The rate of interest was 3% less than what the fund was borrowing at, 3) He failed to disclose the transaction.

Interesting enough, 2 months after the loan was made, Falcone made a personal capital commitment of 10mil to a "non-harbinger fund".

The amounts 113m and 10mil I have seen before, which is why I'm interested in whether this IRS claim is legit. Could that 113.2 mil been used to fund some entity which was going to purchase assets from his fund? Could Falcones personal and separate 10 million commitment to the non-harbinger fund, represent the premium/collateral as part of a swap trade betting against the value of assets held by the entity? I wonder.

Part

2: Harbinger Group Inc

Harbinger Group Inc.

(NYSE: HRG) is a diversified holding company seeking to acquire and to grow

attractive businesses that generate sustainable free cash flow.

What Falcone

essentially did was create this publically traded holding company for which he swapped

the garbage assets out of his funds in exchange for shares in this new

Harbinger Group Inc.

For example,

NEW

YORK, Mar 07, 2011 (BUSINESS WIRE) -- Harbinger Group Inc. ("HGI";

NYSE: HRG) is pleased to announce that it has signed a definitive agreement

today with Harbinger Capital Partners Master Fund I, Ltd.

("Harbinger") for the right to acquire Old Mutual U.S. Life Holdings,

Inc. ("U.S. Life") for $350 million pursuant to an agreement entered

into with OM Group (UK) Limited ("Seller").

http://www.harbingergroupinc.com/phoenix.zhtml?c=118763&p=irol-newsArticle&ID=1536649&highlight=

Here is a timeline of HGI (Click to Enlarge)

Spectrum

Brands Holdings, Old Mutual, and Front Street Re all came from Falcone’s funds.

Acquisition of Fidelity &

Guaranty Life

FG&L: Fidelity

Guarantee & Life is a life insurance and annuity company bought by

Harbinger for $350M from Old Mutual in the spring of 2011. The wholly owned entity

currently has 156 employees and $15.8B under management. The company’s products

are offered throughout the United States using a network of over 300 insurance

marketing organizations (IMOs) that FG&L partners with.

FG&L makes money from the spread between

the interest rates on the annuities they pay out and the rate they make on

their investments. The

company posted an operation loss of $18M in 2011 due to interest rate

violatility which was offset by a “bargain purchase” gain $151M. HGI had

to recognize this gain based on accounting rule SFAS 141R which states that if

during an acquisition, the total acquisition date valuation of the net assets

exceeds that of the considerations transferred, a gain must be marked on the

sale. Essentially,

Harbinger Group judged that FG&L was worth $151M more than they paid.

Per their annual report this judgment was made from, among other things, an

independent appraisal of FG&L and the external pressures to sell

surrounding Old Mutual.

A 151m gain due to a

“bargain purchase”??? There was a recent

short write up about how ridiculous these type of accounting tricks are which

you can find here.

NEED PROFIT? BUY SOMETHING! Jul, 30, 2012

This OM Financial Life Insurance Company, now known as

Fidelity Guarantee & Life Insurance, in my opinion, will be bust within a

year.

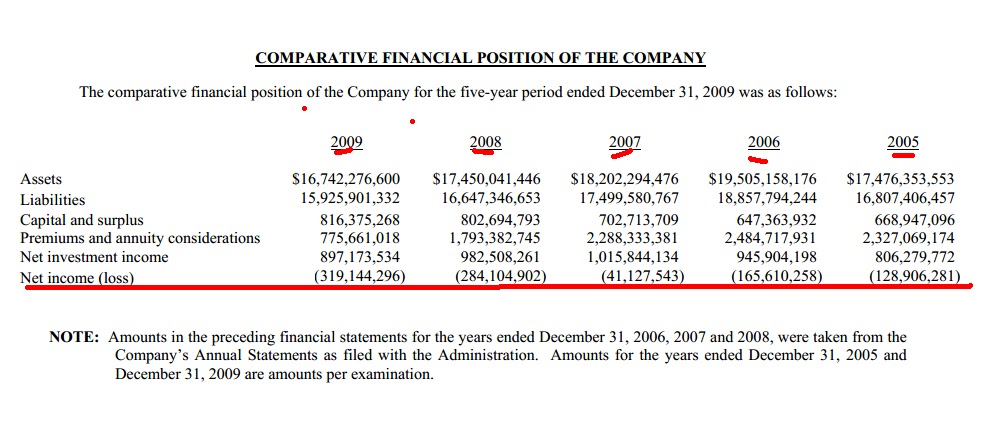

From an Examination

report dated Dec 31, 2009: Notice the losses every year! (Click to Enlarge)

Downgrade of OM

Financial in June 2010, (The same assets deemed a "bargain purchase" a year later)

OM Financial Life’s ratings drop on

concerns about possible sale

June, 3rd 2010

“The downgrade reflects our view of

the nonstrategic nature of OMFL to its parent, Old Mutual PLC, which its parent

demonstrated when it announced its intention to sell the unit,” said Standard

& Poor’s credit analyst Jeremy Rosenbaum in a statement. “In addition, we

are concerned about the impact that OMFL’s narrowing business profile could

have on its long-term business prospects.” OMFL also has significant exposure

to stressed asset classes in its investment portfolio and outsized risk

tolerances, according to the service.

(Coming Soon: I have some great analysis on the holdings of OMFL, which are real cause for concern)

Front Street Re Ltd YIKES!!!!

HGI also announced today that it has

agreed to acquire from Harbinger, FS Holdco Ltd. ("FSH"), the

ultimate parent company of Front Street Re Ltd., a recently formed,

Bermuda-based reinsurer ("Front Street"). The agreement to acquire

FSH contemplates that after closing of the U.S. Life acquisition, a special

committee of the board of directors will consider a proposed $3 billion

reinsurance transaction pursuant to which Front Street would reinsure certain

policy obligations of OM Financial Life Insurance Company, a subsidiary of U.S.

Life, and an affiliate of Harbinger could be appointed as investment manager of

certain of the assets associated with the reinsured business.

(Coming Soon: Formation of Salus Partners--Analysis)

Overpaying for the funds assets, which really shouldn't be a surprise sine Falcone's other fund is the seller.

"HGI is vastly overpaying for the acquisition of assets from its majority and controlling shareholder," according to the suit, which was filed by Harbinger Group investor Alan Kahn in Delaware Chancery Court on Tuesday.

Of the debt raises of

Harbinger Group Inc, I’d like to point out the convertible notes because I’ve

found these to be a common theme in these manipulations. You can bet at some point these are going to

be dropped on HGI like a ton of bricks.

MAY 2011

We completed the private offering

of a sale of $280MM in aggregate of Series A Participating Convertible

Preferred Stock to certain institutional investors.

AUGUST 2011

We completed the private offering

of a sale of $120MM in aggregate of Series A-2 Participating Convertible

Preferred Stock to certain institutional investors. Together with the sale in

May 2011, we raised a total of $400MM in convertible preferred stock

The following filling

makes me wonder about my theory Falcone could be betting against the assets hes

swapping into HGI.

July 20, 2011

Accordingly, each Harbinger Person

reserves the right to change its intentions and develop plans or proposals at

any time, as it deems appropriate. In particular, each Harbinger Person may at

any time and from time to time, (i) in the open market, in privately negotiated

transactions or otherwise, acquire additional Shares or other securities of the

Issuer, including acquisitions from affiliates of the Harbinger Persons; (ii) dispose or transfer of all

or a portion of the securities of the Issuer, including the Shares, that the

Harbinger Persons now own or may hereafter acquire to any person or entity,

including dispositions to affiliates of the Harbinger Persons; (iii) enter into

derivative transactions with institutional counterparties with respect to the

Issuer's securities; (iv) cause or seek to cause the Issuer or any of

its subsidiaries to acquire all or a portion of another person's assets or

business, including acquisitions from affiliates of the Harbinger Persons; (v)

cause or seek to cause the Issuer or any of its subsidiaries to enter into one

or more acquisitions, business combinations or mergers or to sell, transfer or

otherwise dispose of all or any portion of its assets or business to any person

or entity, including acquisitions, business combinations, mergers, sales,

transfers and other dispositions with or to affiliates of the Harbinger

Persons; (vi) restructure the Issuer's or any of its subsidiaries'

capitalization, indebtedness or holding company arrangements; (vii) make

personnel changes to the present management of the Issuer deemed necessary or

desirable; (viii) change the identity of the directors of the Issuer; (ix) make

or propose any other material change in the Issuer's or any of its

subsidiaries' corporate structure or business; or (x) engage in communications

with one or more stockholders, officers or directors of the Issuer and other

persons regarding any of the matters described in clauses (i) through (ix)

above.

Part

3: Spectrum Brands

About:

About Spectrum Brands Holdings, Inc.

Spectrum Brands

Holdings, Inc., a member of the Russell 2000 Index, is a global and

diversified consumer products company and a leading supplier of batteries,

shaving and grooming products, personal care products, small household

appliances, specialty pet supplies, lawn & garden and home pest control

products, personal insect repellents and portable lighting. Helping to meet the

needs of consumers worldwide, the Company offers a broad portfolio of market-leading,

well-known and widely trusted brands including Rayovac®, Remington®, Varta®,

George Foreman®, Black & Decker®, Toastmaster®, Farberware®, Tetra®,

Marineland®, Nature’s Miracle®, Dingo®, 8-in-1®, FURminator®, Littermaid®, Spectracide®, Cutter®,

Repel®, Hot Shot® and Black Flag®. Spectrum Brands Holdings' products are

sold by the world's top 25 retailers and are available in more than one million

stores in more than 120 countries. Spectrum

Brands Holdings generated net

sales of approximately $3.2 billion in fiscal 2011. For more

information, visit www.spectrumbrands.com

Now before you read

the following, I suggest you give this a quick read for its rather interesting

and help put it in perspective.

DELOITTE’S INTANGIBLE ASSET CLIENTS

REVISITED

A

big concern with Spectrum Brands is with how it accounts for acquisitions as well

as future profits. (I believe the numbers below are in millions, its not clear

from the fillings)

Other Acquisitions

During the nine month period ended July 1, 2012, Spectrum

Brands completed the following acquisitions which were not considered significant

individually or collectively:

Black Flag

On October 31, 2011, Spectrum Brands completed the $43,750

cash acquisition of the Black Flag and TAT trade names (“Black Flag”) from The

Homax Group, Inc., a portfolio company of Olympus Partners. The Black Flag and

TAT product lines consist of liquids, aerosols, baits and traps that control

ants, spiders, wasps, bedbugs, fleas, flies, roaches, yellow jackets and other

insects. In accordance with ASC Topic 805, Business

Combinations (“ASC 805”),

Spectrum Brands accounted for the acquisition by applying the acquisition

method of accounting.

The results of Black Flag’s operations since October 31, 2011

are included in the accompanying Condensed Consolidated Statements of

Operations. The purchase

price of $43,750 has been allocated to the acquired net assets, including

$25,000 of identifiable intangible assets, $15,852 of goodwill, $2,509 of

inventories, and $389 of properties and other assets, based upon a preliminary

valuation. Spectrum Brands’ estimates and assumptions for this

acquisition are subject to change as Spectrum Brands obtains additional

information for its estimates during the measurement period. The primary areas

of the acquisition accounting that are not yet finalized relate to certain

legal matters and residual goodwill.

FURminator

On December 22, 2011, Spectrum Brands completed the $141,745

cash acquisition of FURminator, Inc. (“FURminator”) from HKW Capital Partners

III, L.P. FURminator is a leading worldwide provider of branded and patented

pet deshedding products. In accordance with ASC 805, Spectrum Brands accounted

for the acquisition by applying the acquisition method of accounting.

The results of FURminator operations since December 22, 2011

are included in the accompanying Condensed Consolidated Statements of

Operations. The purchase

price of $141,745 has been allocated to the acquired net assets, including

$79,000 of identifiable intangible assets, $68,531 of goodwill, $9,240 of

current assets, $648 of properties and $15,674 of current and long-term

liabilities, based upon a preliminary valuation. Spectrum Brands’

estimates and assumptions for this acquisition are subject to change as

Spectrum Brands obtains additional information for its estimates during the

measurement period. The primary areas of the acquisition accounting that are

not yet finalized relate to certain legal matters, income and non-income based

taxes and residual goodwill.

Look at the write

downs to intangibles and goodwill back in 2007-2009, a good indicator for what

lies ahead?

During fiscal 2009, 2008, 2007 and 2006, pursuant to the Financial Accounting Standards Board Codification Topic 350: “Intangibles-Goodwill and Other,” formerly the Statement of Financial Accounting Standards No. 142, “Goodwill and Other Intangible Assets,” Spectrum conducted its annual impairment testing of goodwill and indefinite-lived intangible assets. As a result of these analyses Spectrum recorded non-cash pretax impairment charges of approximately $34 million, $861 million, $362 million and $433 million in the eleven month period ended August 30, 2009, fiscal 2008, fiscal 2007 and fiscal 2006, respectively. See the “Critical Accounting Policies—Valuation of Assets and Asset Impairment” section of http://www.sec.gov/Archives/edgar/data/1487730/000119312510070095/ds4.htm

The following treatment of “Cost of goods sold” and

“Selling, general and administrative expenses,” seem inappropriate?

Restructuring and Related Charges

The Company reports restructuring

and related charges associated with manufacturing and related initiatives of

Spectrum Brands in “Cost

of goods sold.” Restructuring and related charges reflected in “Cost of

goods sold” include, but are not limited to, termination, compensation and related costs

associated with manufacturing employees, asset impairments relating to manufacturing

initiatives, and other costs directly related to the restructuring or

integration initiatives implemented.

The Company reports restructuring

and related charges relating to administrative functions of Spectrum Brands in

“Selling, general and administrative expenses,” such as initiatives impacting

sales, marketing, distribution, or other non-manufacturing functions.

Restructuring and related charges reflected in “Selling, general and administrative expenses”

include, but are not limited to, termination and related costs, any asset impairments relating to the functional areas

described above, and other costs directly related to the initiatives

Unusual growth in

subsidiaries: Given the huge quantities of Goodwill and Other Intangibles

picked up and written down over this time, is it possible some of these off

balance sheet entities could be holding distressed paper assets?

Dec 2005: 5 Subsidiaries

Dec 2007: 95 Subsidiaries

Dec 2011: 135 Subsidiaries

Will history repeat

itself? Not only in terms of the

goodwill and intangible write-downs of Spectrum Brands, but another pump and

dump orchestrated by Philip Falcone?

On February 3,

2009, Spectrum and thirteen of its United States subsidiaries (collectively,

the “Debtors”) filed voluntary petitions for reorganization under Chapter 11 of

the United States Bankruptcy Code in the United States Bankruptcy Court for the

Western District of Texas. On August 28, 2009, the Debtors’ joint plan of

reorganization (the “Plan”) became effective and the Debtors emerged from

Chapter 11 of the Bankruptcy Code. Pursuant to the Plan, Spectrum’s capital

structure was realigned. Spectrum’s outstanding equity securities were

cancelled with no distribution to holders of Spectrum’s then existing equity.

Spectrum issued new common stock and 12% Senior Subordinated Toggle Notes due

2019 (“PIK Notes”) to holders of allowed claims in respect of Spectrum’s then

outstanding public senior subordinated notes.

(Coming Soon more spectrum brands analysis)

In conclusion, Harbinger

Group Inc is holding greater than a billion dollars of shit Falcone couldn’t

wait to get off his hands.

Short Side Risk:

As far as shorts go the risk that a buyout such as Harbin Electric

or (tentative) Focus media, I feel are quite small. HGI and Spectrum are prime candidates for

collapse, and that is the plan in my opinion.

Having studied and followed the flows I believe I understand why certain

concerns are more sensitive to their plans being exposed.

Falcone and the trust could continue to mark this thing up

on insider buying and bogus revenue numbers which never will materialize, but I

feel the risk reward is good here especially if you pyramid on the way down.

Another way to mitigate risk on the short side might be to

contact the bond holders of Harbinger as well as Spectrum regarding these

concerns; i.e. enron style accounting and the self dealing Philip Falcone.

Some Bond Holders of this Junk: (How these guys get away selling this stuff to the state is beyond me...Guess when no one goes to jail why not, right?)

Data for July 2011 - State of New Jersey

HARBINGER GROUP INC 11/15 FIXED 10.625 575,301.22

June, 2012 - Vermont State Treasurer

HARBINGER GROUP INC '41146AAB2 $1,000,000

SPECTRUM BRANDS INC '84762LAG0 $1,975,000

GS HIGH YIELD FUND - Goldman Sachs

SPECTRUM BRANDS INC $2,050,000 (6.75%)SPECTRUM BRANDS INC $5,450,000 (9.5%)

SPECTRUM BRANDS INC $13,650,000.00 (9.5% different issue)

Holdings - Prudential Investments

Spectrum Bonds

Some Bond Holders of this Junk: (How these guys get away selling this stuff to the state is beyond me...Guess when no one goes to jail why not, right?)

Data for July 2011 - State of New Jersey

HARBINGER GROUP INC 11/15 FIXED 10.625 575,301.22

June, 2012 - Vermont State Treasurer

HARBINGER GROUP INC '41146AAB2 $1,000,000

SPECTRUM BRANDS INC '84762LAG0 $1,975,000

GS HIGH YIELD FUND - Goldman Sachs

SPECTRUM BRANDS INC $2,050,000 (6.75%)SPECTRUM BRANDS INC $5,450,000 (9.5%)

SPECTRUM BRANDS INC $13,650,000.00 (9.5% different issue)

Holdings - Prudential Investments

Spectrum Bonds

And maybe even people like this;

Wisconsin Economic Development Corp; 4 Mil in Contingent Exposure

Wisconsin Economic Development Corp gives Spectrum grants 4M incentive

for spectyrum to move to winsconson, in exchange for its promise to keep its 470 existing Dane County

employees through Sept. 30, 2016, and invest $40 million in its Wisconsin

operations by that time. If it fails to fulfill these requirements, it must pay

back the $4 million with interest. Otherwise, it owes nothing beyond an $80,000

origination fee.

Disclaimer:

The author of this piece is not an investment professional

and may be short mentioned securities. Everything presented is done so

using public sources and believed to be true.

Kmart has an opening for you Donny....because you clearly have no idea what you are talking about. You will have to talk to Falcone about the SEC issue but as it relates to SPB and HRG, the value is there. I think you need to brush up on your accounting.

ReplyDeleteValue is there? Like the value was there in 2005 before the 1.5B in write downs (06,07,08,09) to good will and intangible assets?

ReplyDelete